Thanks to the high tech smartphones in our pockets, there are so many great apps available for saving and investing money. Whether you use an Apple phone or an Android phone, these devices can really improve your personal finances. There are smartphone apps available which can be used for banking, stock investing, crypto investing, stock option trading, futures trading, and more. Some apps even provide all of these services! Fortunately, many of these apps are simple and intuitive to operate for even the most basic user.

Currently, my favorite personal finance smartphone app is called Robinhood. The Robinhood app is like a financial swiss army knife in your pocket. This app allows you to buy stocks, ETFs, options, crypto, futures, and wager on prediction markets. Robinhood changed the investing game when it entered the market in 2013 by offering retail investors commission free trading. At that time, most of the brokerages were charging between $5-$10 per trade! Those fees added up quickly hurting small and large retail investors portfolios. Thankfully, when Robinhood started becoming popular, the other brokerages copied Robinhood’s offering of commission free trading as well. Now, nearly all of the major brokerages offer commission free trading, so I would like to tip my hat to Robinhood for bringing this benefit to the market!

These days, Robinhood’s business and product suite have grown substantially. Robinhood is no longer a small startup company and their business is currently worth just over $100 billion. Robinhood now even offers credit cards and mortgages (mortgages are offered through a partner company). Additionally, if you sign up for Robinhood Gold, which costs $5 per month or $50 annually, subscribers receive 3.5% interest annually on their idle cash. This rate is much better than the rate that I receive in my bank account so it is definitely an attractive offer. This interest rate does fluctuate throughout the year based on borrowing and lending rates typically influenced by the Federal Reserve. In early 2025, the interest rate that I was receiving on my cash was 4%, but the Fed has been lowering interest rates this year which has impacted the rate that Robinhood can pay to its customers. The other great thing about the cash that you store on Robinhood is it is FDIC insured up up to $2.5 million dollars “at partner banks.” This gives me that warm and fuzzy feeling that my money is safe sitting in my Robinhood brokerage account!

Here is a quick and shameless referral pitch from me. If you sign up for Robinhood using my referral link here: https://join.robinhood.com/brianh850 we can both receive a stock valued from $5-$200.

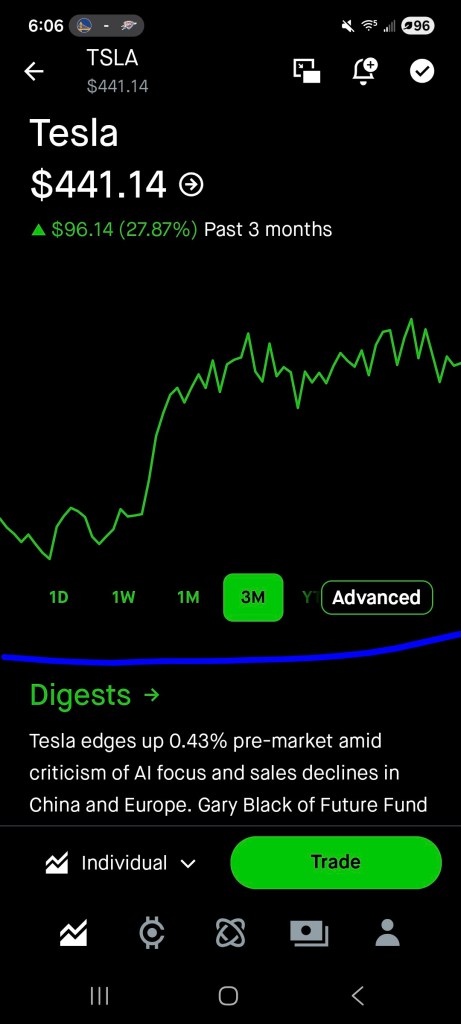

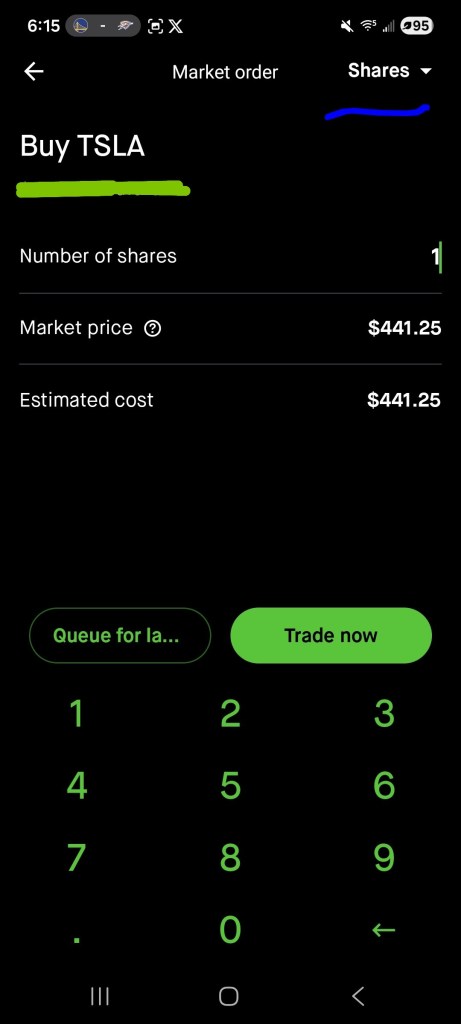

As mentioned above, you can also buy individual stocks and ETFs through the Robinhood app. The app makes it super easy to buy and sell investments. I personally utilize Robinhood as my brokerage account to help me execute investments and trade ideas on the go. Maybe I am reading an article on CNBC about an interesting stock, ETF, or IPO that I want to make an investment in. After performing some research, I log into the Robinhood app and execute a purchase. Below is a screenshot of what the Robinhood app looks like on an Android phone (Apple will look very similar). In the screenshot, I am viewing Tesla stock, ticker symbol TSLA, which is trading at $441.14 per share on November 12, 2025. I am viewing the 3 month chart and I can easily switch chart timeframes using the timeframe selections that I underlined in blue.

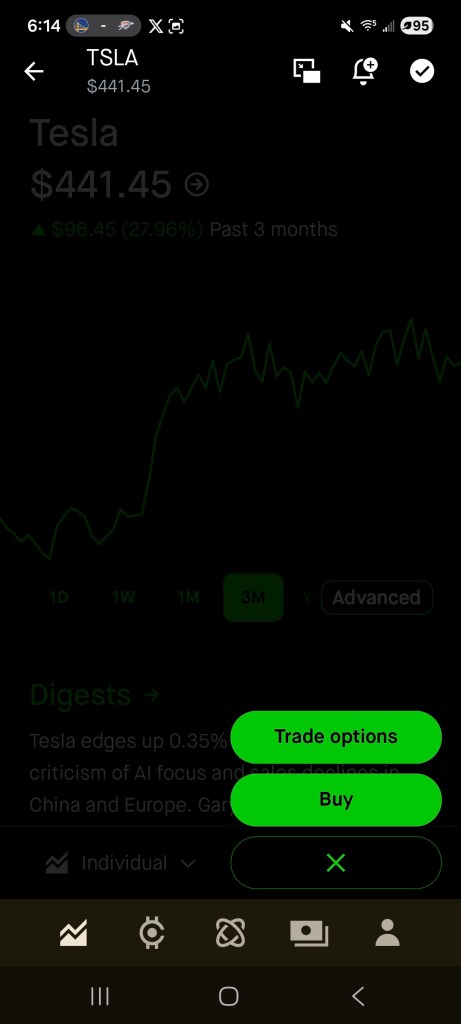

If I was ready to purchase Tesla stock I would perform the following:

- Tap the “Trade” button

- Select “Buy”

- Input the number of shares that I want to purchase and select “Trade Now” (Note: by tapping where it says “Shares” I can customize my order further)

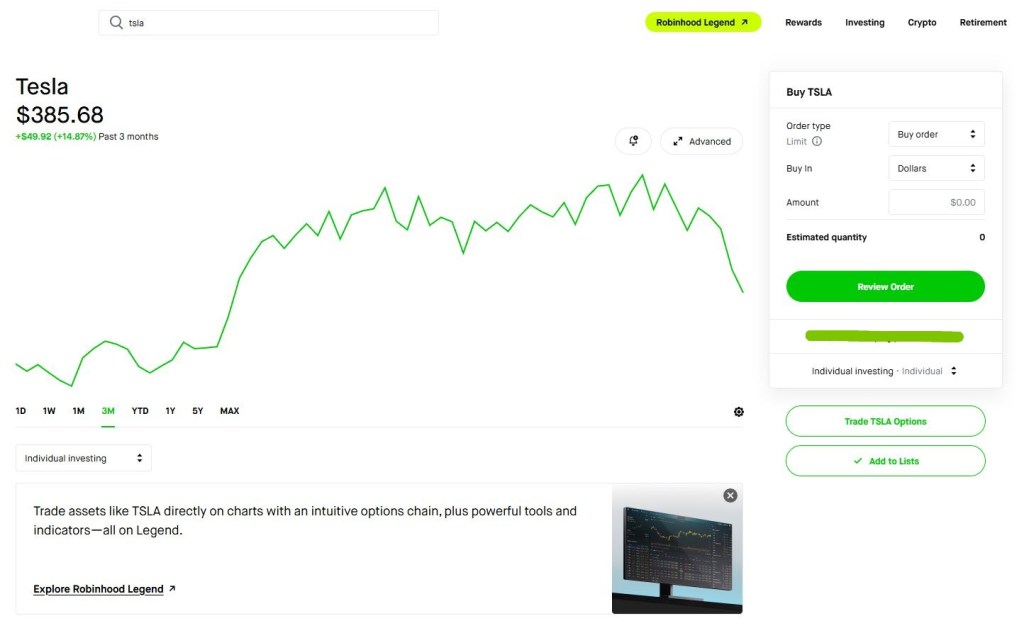

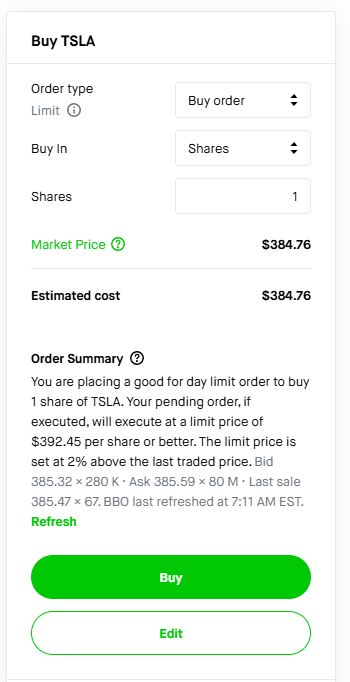

You can see how simple that was to buy a stock on the Robinhood app, which is why the company currently has 26 million customers. If you prefer not to make your investments using your smartphone, Robinhood also allows you to buy and sell investments on your desktop or laptop computer. See the screenshots below to view how the website interface looks when buying Tesla on a desktop computer:

As you can see, the desktop app looks slightly different from the smartphone app and it gives you a larger screen to work with. Regardless, whether you are investing from a smartphone or via a computer, the process is simple and intuitive.

In addition to investing in stocks, over the last two years I have been utilizing trading call and put options in my Robinhood account as a more speculative strategy. I have seen some decent success with trading stock options, so I am continuing to experiment with them further. Essentially a stock option gives you the right, but not an obligation, to buy or sell a stock at a specific price. You pay a premium for this right, but the percentage moves on options are much larger than just buying a singular stock. For example, a stock price may move up 10% in a day while the stock option may move up 40%. There are more advanced option strategies than simply buying call or put options. For the time being, I am sticking with what I know. It can be easy to make or lose a lot of money while trading options, but you must weigh that risk with your investment strategy and money goals.

Now, let’s talk a little bit about crypto trading and investing. As mentioned earlier, Robinhood does allow you to buy and sell select cryptocurrencies. At the moment, Robinhood has a much more limited crypto menu when compared to some of the other pure play crypto exchanges like Coinbase. That can be a good or a bad thing depending on your needs. If you’re a crypto guru, you may want to look into using a crypto only exchange. If you are a novice to moderate crypto investor, Robinhood should have enough options. As of today, November 12, 2025, Robinhood currently allows for the buying and selling of 45 different cryptocurrencies. Below is a list of some of the more popular cryptocurrencies available for trading on Robinhood:

- Uniswap

- Solana

- Avalanche

- Bitcoin

- Cardano

- Dogecoin

- Binance Coin

- Ethereum

- Ripple or XRP

- Chainlink

- Hyperliquid

- Aster

- Litecoin

- Arbitrum

- Official Trump

- USDC

- World Liberty Financial

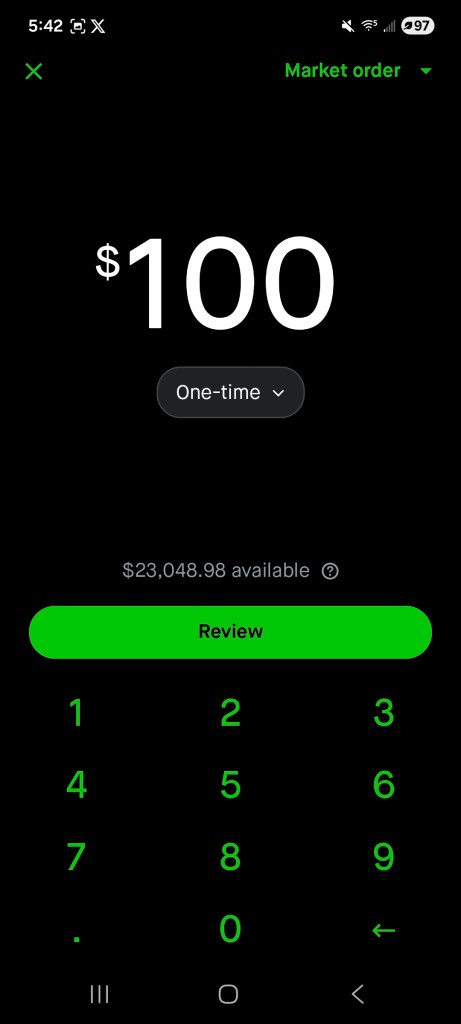

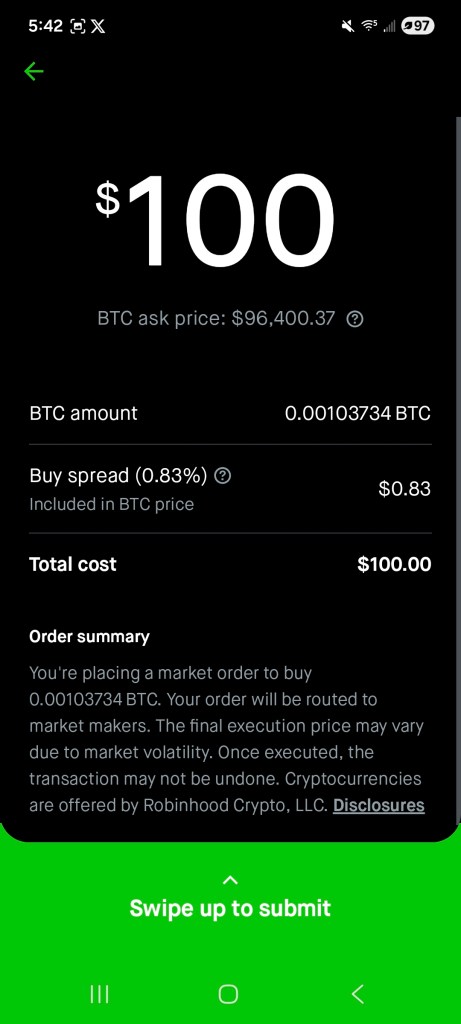

Buying or selling crypto on Robinhood is as simple as buying or selling stocks. Below is an example of buying Bitcoin via an Android phone using the Robinhood app:

- Tap the “Buy” button

- Input the dollar amount or number of Bitcoins (or fractions) that I want to buy and select “Review”

- “Swipe up to submit” order

Quick and easy process!

Another crypto feature to note, in many states Robinhood allows staking with Ethereum and Solana. This means that by helping secure the network, just by clicking “Stake” on your crypto holdings, you can receive a small yield on your crypto. Presently, if you stake Ethereum, you earn 2.09% annually and staking Solana yields 4.60% annually. Staking can be a helpful tool to earn passive yield if you are a long term holder of a specific cryptocurrency. It looks like Robinhood might roll out staking to more cryptocurrencies in the future, so be on the lookout for that.

The last high powered investing feature that I want to mention is Robinhood’s current IRA match offer. If you open an IRA with Robinhood, they will match your annual contributions up to 3% if you are a Robinhood Gold subscriber and up to 1% if you are a non Gold subscriber. This is huge if you are a small business owner, freelancer, or if you work for a company that does not offer a retirement matching program. Retirement matching programs can help you grow your money quicker and Robinhood is helping a lot of investors with this feature.

As you can see, Robinhood is certainly a powerful and innovative personal finance app. I have been a happy Robinhood customer since 2017 and it has been great to watch them grow as a company. Robinhood seems to always be looking for new ways to improve their product offerings and satisfy their customers. This is why I crowned them “My Favorite Smartphone App for Saving and Investing.” Well done Robinhood team, please continue to “Democratize Finance” for us all!

If you sign up for Robinhood using my referral link here: https://join.robinhood.com/brianh850 we can both receive a stock valued from $5-$200.